How to Buy Your First House in Malaysia: Complete 2026 Guide

Buying your first house in Malaysia is one of the most significant financial decisions you will ever make. Whether you are a fresh graduate saving your first paycheck or a young professional eyeing that dream condo, the process can feel overwhelming. From calculating your budget and checking your loan eligibility to signing the Sale and Purchase Agreement (SPA) and collecting your keys, there are many moving parts.

This guide walks you through every step of the house-buying process in Malaysia for 2026. We cover the latest government schemes, updated stamp duty exemptions, EPF withdrawal rules, and financing options so you can move forward with confidence. By the end, you will have a clear roadmap from "I want to buy a house" to "I have the keys."

Step 1: Determine Your Budget and Affordability

Before you browse a single listing, you need to understand how much house you can realistically afford. The biggest mistake first-time buyers make is falling in love with a property that is out of their financial reach.

The One-Third Income Rule

A widely accepted guideline is that your monthly mortgage payment should not exceed one-third of your gross monthly income. If you earn RM5,000 per month, aim for a maximum instalment of around RM1,650. This leaves enough room for other expenses, savings, and emergencies.

Total Cost Beyond the Purchase Price

The sticker price of a property is only part of the picture. You need to budget for several upfront and ongoing costs:

| Cost Component | Estimated Amount |

|---|---|

| Down payment | 10% of property price |

| SPA legal fees | 0.5%–1% of property price |

| Loan agreement legal fees | 0.5%–1% of loan amount |

| Stamp duty (MOT) | 1%–4% (tiered; exemptions may apply) |

| Stamp duty (loan agreement) | 0.5% of loan amount |

| Valuation fees (subsale) | RM200–RM1,500 |

| Insurance / takaful (MRTA/MLTA) | Varies by age and loan amount |

| Renovation and furnishing | RM10,000–RM80,000+ |

| Maintenance fees (strata) | RM150–RM500/month |

For a RM400,000 property, your total upfront cash outlay (excluding the loan) can easily reach RM50,000–RM70,000 once you factor in the down payment, legal fees, stamp duty, and basic furnishing.

Use our Home Loan & DSR Calculator to estimate your monthly repayments and check whether your Debt Service Ratio falls within the bank's threshold.

Step 2: Check Your Home Loan Eligibility

Banks do not just look at your salary when deciding whether to approve a mortgage. They assess your overall creditworthiness using several criteria.

Debt Service Ratio (DSR)

Your DSR measures how much of your net income goes toward debt repayments. Most Malaysian banks cap the DSR at 60%–70%, though some allow up to 75% for higher-income borrowers. The formula is:

DSR = (Total monthly debt obligations / Net monthly income) x 100%

If your DSR is too high, you either need to reduce existing debts or look at a cheaper property.

CCRIS and CTOS: Your Credit Report

Before applying for a loan, pull your own credit report from CCRIS (Central Credit Reference Information System, managed by Bank Negara Malaysia) and CTOS. These reports show your repayment track record for credit cards, personal loans, car loans, PTPTN, and any other borrowings. Late payments or defaults will significantly hurt your loan approval chances.

As of 2026, you can check your CCRIS report free of charge via the Bank Negara Malaysia eCCRIS portal, and CTOS offers a free basic report once per year.

Pre-Approval: A Smart First Move

Consider getting a loan pre-approval before you start house hunting. A pre-approval letter from a bank tells you the maximum amount you can borrow and shows sellers and agents that you are a serious buyer. It typically involves submitting your income documents and consenting to a credit check.

Key documents for loan application:

- Copy of IC (front and back)

- Latest 3–6 months payslips

- Latest 3–6 months bank statements

- EPF statement (to show savings history)

- EA form / BE form (income tax)

- Letter of employment

- Existing loan commitment documents

For a deeper dive into choosing the right financing, read our Home Loan Guide.

Step 3: Use Your EPF (KWSP) for the Down Payment

One of the biggest hurdles for first-time buyers is coming up with the cash for the 10% down payment. The good news is that you can use your Employees Provident Fund (EPF/KWSP) savings to help cover it.

Account 2 Withdrawal for Housing

EPF members below age 55 can withdraw from their Account 2 (now the Flexible Account under the EPF restructuring) for the purpose of purchasing or building a residential property. The withdrawal amount is generally calculated as:

Eligible withdrawal = Property price minus loan amount (capped at Account 2 balance)

For example, if you are buying a RM400,000 house with a 90% loan (RM360,000), you can withdraw up to RM40,000 from Account 2, subject to your available balance.

How to Apply via i-Akaun

- Log in to your EPF i-Akaun online

- Select the housing withdrawal category

- Upload your SPA, loan offer letter, and IC copy

- EPF processes the application within 2–4 weeks

- Funds are disbursed to the relevant party (developer/seller/bank)

Important Timing Note

EPF withdrawals take 2–4 weeks to process, but booking fees and earnest deposits are typically due immediately when you reserve a property. You will likely need to pay the initial booking fee (2%–3%) in cash first, then use your EPF withdrawal to cover the remaining down payment portion.

For a full walkthrough on EPF housing withdrawals, including eligibility requirements and common pitfalls, see our EPF Withdrawal Guide.

Step 4: Choose the Right Property Type

Malaysia offers a wide range of property types, and the right choice depends on your budget, lifestyle, and long-term plans.

Condominium vs Landed Property

| Factor | Condominium / Apartment | Landed (Terrace, Semi-D, Bungalow) |

|---|---|---|

| Price (entry level) | RM250K–RM500K in KL/Selangor | RM400K–RM800K in KL/Selangor |

| Maintenance | Monthly fees (RM150–RM500+) | Self-maintained |

| Facilities | Pool, gym, security | Usually none (gated communities vary) |

| Land ownership | Strata title (shared land) | Individual title |

| Appreciation potential | Moderate | Generally higher for well-located lots |

Freehold vs Leasehold

Freehold properties give you indefinite ownership of the land. Leasehold properties are held for a fixed term (typically 99 years), after which the land reverts to the state government unless the lease is renewed. Leasehold properties are generally 15%–25% cheaper than comparable freehold ones, but they may be harder to sell or refinance as the remaining lease decreases. Banks may also impose stricter loan conditions for leasehold properties with fewer than 60 years remaining.

New Launch vs Subsale: Which Is Better for First Timers?

This is one of the most common questions among first-time buyers. Each option has distinct advantages.

| Factor | New Launch (Under Construction) | Subsale (Completed Property) |

|---|---|---|

| Price | Developer pricing, potential early-bird rebates | Market-driven, negotiable |

| Down payment | Often 0%–5% with developer absorptions | Typically 10% |

| Move-in timeline | 2–4 years (construction period) | 2–3 months (loan + legal process) |

| Condition | Brand new, with 24-month defect liability period | Used; inspect thoroughly before buying |

| Loan interest during construction | Progressive interest payments (DIBS banned) | Full instalment starts after loan disbursement |

| Choice of unit/layout | More options if buying early | Limited to what is on the market |

| Risk | Developer may delay or face issues | What you see is what you get |

For first-time buyers on a tight cash flow, new launches with developer rebates and lower upfront costs can be attractive. However, if you need to move in quickly or want to see exactly what you are getting, a subsale property is the safer bet.

For a detailed comparison, read our Subsale vs New Launch Guide.

Step 5: Secure Your Home Loan

Once you have identified a property and confirmed your budget, it is time to lock down financing. Apply to at least 3–4 banks to compare offers.

Standardised Base Rate (SBR) in 2026

Since 2022, Malaysian home loans have been priced against the Standardised Base Rate set by Bank Negara Malaysia. As of early 2026, the SBR across most banks sits at around 3.00%, with effective home loan rates (SBR + spread) typically ranging from 3.80% to 4.50% depending on the bank and your risk profile.

Fixed Rate vs Variable Rate

| Feature | Variable Rate (SBR-based) | Fixed Rate |

|---|---|---|

| Interest rate | Fluctuates with OPR changes | Locked in for a set period (e.g., 5–10 years) |

| Monthly instalment | May increase or decrease | Stays the same during the fixed period |

| Who is it for? | Borrowers comfortable with some rate risk | Borrowers who want predictable payments |

| Availability | All banks | Limited offerings |

Most Malaysian borrowers opt for variable-rate loans because they are widely available and historically competitive. However, if you prefer certainty in your monthly budget, explore fixed-rate options available at select banks.

Islamic Financing vs Conventional Loans

Malaysia is one of the world's leading Islamic finance markets. Islamic home financing products (such as Musharakah Mutanaqisah or Bai Bithaman Ajil) do not charge "interest" but instead use profit-rate structures that achieve a similar economic outcome. Key differences include:

- Islamic financing has a ceiling profit rate, meaning your rate will never exceed a declared maximum

- Conventional loans may have compounding interest on arrears, while Islamic products typically do not

- Both are regulated by Bank Negara Malaysia and are equally valid for property purchases

Choose the product that aligns with your financial preferences and beliefs. For more details, see our Home Loan Guide.

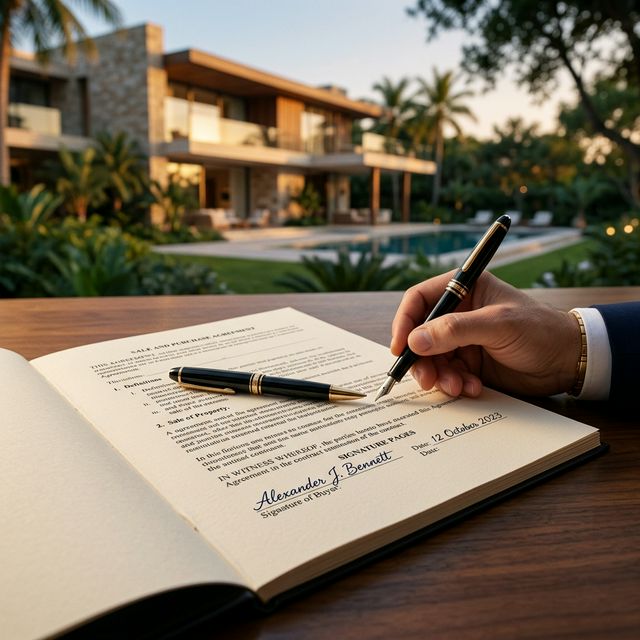

Step 6: Sign the SPA (Sale and Purchase Agreement)

The SPA is the most critical legal document in your property purchase. It binds both buyer and seller to the agreed terms.

What Is the SPA?

The Sale and Purchase Agreement sets out the property details, purchase price, payment schedule, completion date (for new launches), and the obligations of both parties. For new development projects, the SPA follows a standard format prescribed by the Housing Development (Control and Licensing) Act 1966 (Schedule G for landed properties, Schedule H for strata). For subsale properties, the SPA is drafted by the appointed lawyer.

Key Clauses to Watch

- Completion / Vacant Possession Date: For new launches, the developer must deliver vacant possession within 24 months (landed) or 36 months (strata) from the SPA date. Delays trigger Liquidated Ascertained Damages (LAD) payable to you.

- Defect Liability Period: 24 months from vacant possession, during which the developer must repair defects at no cost to you.

- Late Payment Interest: If you fail to make payments on time, the SPA will specify the interest rate charged on overdue amounts.

- Termination Clauses: Conditions under which either party can exit the agreement.

SPA Timeline

- You sign the SPA and pay the balance of the deposit (usually within 14 days of booking)

- Your lawyer stamps the SPA at LHDN

- The bank disburses the loan to the seller/developer

- For new launches, progressive payments follow the construction schedule

- For subsale, the full balance is typically settled within 90 days (or as extended by agreement)

For a complete breakdown of what to check before signing, read our SPA Agreement Guide.

Step 7: Pay Stamp Duty and Legal Fees

This step is where many first-time buyers get surprised by the costs. Understanding the fees upfront helps you avoid last-minute cash shortfalls.

Stamp Duty on Memorandum of Transfer (MOT)

Stamp duty is a tax paid to the government when property ownership is transferred. In 2026, the rates for Malaysian citizens and permanent residents are:

| Property Value | Stamp Duty Rate |

|---|---|

| First RM100,000 | 1% |

| RM100,001–RM500,000 | 2% |

| RM500,001–RM1,000,000 | 3% |

| Above RM1,000,000 | 4% |

Example: For a RM500,000 property, the MOT stamp duty is:

- RM100,000 x 1% = RM1,000

- RM400,000 x 2% = RM8,000

- Total: RM9,000

Stamp Duty on Loan Agreement: 0.5% of the loan amount. For a RM450,000 loan, that is RM2,250.

First-Time Buyer Stamp Duty Exemption (Extended to December 2027)

As announced in Budget 2025 and extended through 2027, first-time Malaysian homebuyers purchasing properties priced up to RM500,000 are eligible for 100% exemption on the MOT stamp duty. This can save you up to RM9,000. Properties priced between RM500,001 and RM1,000,000 receive a tiered partial exemption.

Lawyer Fees

Legal fees for the SPA and loan agreement follow a scale set by the Solicitors' Remuneration Order:

| Property/Loan Value | Fee Rate |

|---|---|

| First RM500,000 | 1.0% |

| RM500,001–RM1,000,000 | 0.8% |

| RM1,000,001–RM3,000,000 | 0.7% |

| RM3,000,001–RM5,000,000 | 0.6% |

| Above RM5,000,000 | 0.5% |

Note: You will typically need two sets of legal fees — one for the SPA and one for the loan agreement. Some lawyers offer package deals. Additional disbursements (stamp duty adjudication, registration, search fees) add RM1,000–RM3,000.

For full calculations and examples, see our Stamp Duty Guide and Legal Fees Guide.

Step 8: Complete Transfer and Get Your Keys

This is the final stretch. The exact process varies depending on whether you bought a new launch or subsale property.

For Subsale Properties

- Your lawyer registers the Memorandum of Transfer (MOT) at the relevant land office

- Transfer of ownership is recorded on the property title

- The seller hands over vacant possession once the full purchase price is settled

- Transfer utilities (TNB for electricity, water supply, internet) to your name

- Collect your keys and conduct a thorough inspection of the property

For New Launch Properties

- The developer notifies you when construction reaches the stage for Vacant Possession (VP)

- You receive a Notice of Vacant Possession along with a VP checklist

- Conduct a defect inspection — check walls, flooring, plumbing, electrical fittings, doors, and windows

- Submit a defect report to the developer within 30 days

- The developer has 30 days to rectify reported defects

- The 24-month Defect Liability Period begins from the date of VP

- Transfer or set up utility accounts (TNB, water, Unifi/broadband)

- Apply for renovation permits from the management office if you plan to do any works

Defect Inspection Tips

- Bring a checklist: check every power outlet, tap, light switch, and door lock

- Look for cracks, uneven tiling, water stains (signs of leaks), and paint defects

- Test water pressure in all bathrooms and the kitchen

- Check that the floor area matches what was promised in the SPA

- Take photos and videos of every defect as evidence

Government Schemes for First-Time Buyers 2026

The Malaysian government offers several programmes to make homeownership more accessible, especially for first-time buyers and lower-income households.

Key Schemes Available in 2026

| Scheme | Eligibility | Key Benefit |

|---|---|---|

| PR1MA (Perumahan Rakyat 1Malaysia) | Household income RM2,500–RM15,000/month | Affordable homes priced 20%–30% below market |

| SJKP (Skim Jaminan Kredit Perumahan) | No fixed income / informal sector workers | Government-guaranteed home loan |

| RUMAWIP | Single income up to RM10,000/month in KL | Affordable housing units in Kuala Lumpur |

| Stamp Duty Exemption (First-Time Buyer) | First residential property up to RM500,000 | 100% MOT stamp duty waiver (extended to Dec 2027) |

| My First Home Scheme (Skim Rumah Pertamaku) | Income up to RM10,000/month, property up to RM500,000 | Up to 110% financing (no 10% down payment required) |

Skim Rumah Pertamaku is particularly valuable because it allows eligible buyers to get a loan covering the full purchase price plus some incidental costs, effectively eliminating the 10% down payment barrier that stops many young Malaysians from entering the market.

State-Level Incentives

Some states offer additional benefits. For example, Selangor has the Rumah Selangorku programme for affordable housing, while Penang provides the Penang Affordable Housing scheme. Check with your state government's housing authority for localised programmes.

For a comprehensive breakdown of all available schemes, read our Government Housing Schemes Guide.

First-Time Buyer Checklist: Full Cost Summary Table

Here is a consolidated checklist of every cost you should budget for when buying your first house in Malaysia. We use a RM400,000 property with a 90% loan (RM360,000) as a reference example.

| Step | Item | Estimated Cost (RM400K Property) |

|---|---|---|

| 1 | Booking fee / earnest deposit (2%–3%) | RM8,000–RM12,000 |

| 2 | Balance of down payment (10% minus booking) | RM28,000–RM32,000 |

| 3 | SPA legal fees (approx. 1% + disbursements) | RM4,500–RM5,500 |

| 4 | SPA stamp duty (RM10 nominal) | RM10 |

| 5 | MOT stamp duty (may be exempted for first-timer) | RM0–RM5,000 |

| 6 | Loan agreement legal fees | RM3,500–RM4,500 |

| 7 | Loan agreement stamp duty (0.5% of loan) | RM1,800 |

| 8 | Valuation fees (subsale only) | RM800–RM1,500 |

| 9 | MRTA / MLTA insurance or takaful | RM5,000–RM15,000 |

| 10 | Fire insurance / takaful (annual) | RM200–RM500 |

| 11 | Renovation and furnishing | RM15,000–RM50,000+ |

| 12 | Utility deposits (TNB, water) | RM500–RM1,000 |

| Total estimated upfront cost | RM67,310–RM127,310 |

Note: If you qualify for the first-time buyer stamp duty exemption on a property up to RM500,000, your MOT stamp duty could be RM0, reducing the total significantly. EPF withdrawals can offset a large portion of the down payment and even some recurring loan payments.

Monthly Ongoing Costs

| Item | Estimated Monthly Cost |

|---|---|

| Mortgage instalment (RM360K, 35 years, ~4.2%) | RM1,600–RM1,750 |

| Maintenance / sinking fund (condo) | RM150–RM400 |

| Assessment tax (cukai taksiran) | RM50–RM150 |

| Quit rent (cukai tanah) | RM10–RM50 |

| Home insurance / takaful (monthly equivalent) | RM20–RM50 |

FAQs About Buying Your First House in Malaysia

Q: How much deposit do I need to buy a house in Malaysia?

For most properties, you need a 10% down payment. This is typically split into a 2%–3% booking fee (paid immediately when you reserve the property) and the remaining 7%–8% due within 14 days of signing the SPA. However, if you qualify for the My First Home Scheme (Skim Rumah Pertamaku), you may get up to 110% financing, meaning no down payment is required. First-time buyers can also use their EPF Account 2 savings to cover part or all of the down payment.

Q: Can I buy a house in Malaysia with a salary of RM3,000?

Yes, but your options will be limited. With a RM3,000 gross salary and no other debts, a bank might approve a loan of approximately RM150,000–RM200,000, depending on your DSR. This puts you in the range of affordable housing schemes like PR1MA or RUMAWIP. Focus on properties below RM250,000 in areas with lower price points, or consider the SJKP loan guarantee scheme if you do not have a fixed income proof. You can also apply jointly with a spouse or family member to increase borrowing capacity.

Q: How long does it take to buy a house in Malaysia from start to finish?

For a subsale property, the process from booking to collecting keys typically takes 3–4 months. This includes loan approval (2–4 weeks), SPA execution and legal work (4–6 weeks), and loan disbursement to the seller (2–4 weeks). For a new launch property, you sign the SPA and then wait 2–4 years for construction to complete before receiving vacant possession. The legal and loan process at the front end is similar, but the wait for the finished property is much longer.

Q: What credit score do I need to get a home loan in Malaysia?

Malaysia does not use a single universal credit score like some other countries. Banks assess your CCRIS report (which shows your repayment history over the past 12 months) and CTOS score. Generally, you want zero outstanding "1" or "2" marks on CCRIS, which indicate late payments. Your CTOS score should ideally be above 697 (rated "good" or higher). If you have a PTPTN loan, ensure it is being repaid on schedule, as defaults will appear on your credit record and are a common reason for loan rejection among younger buyers.

Q: Can I use EPF to pay for my first house?

Yes. EPF members can withdraw from Account 2 (or the Flexible Account under the new EPF structure) to purchase a residential property. The withdrawal can be used for the down payment, to reduce the loan principal, or even for monthly instalment payments. You must have a signed SPA and a loan offer letter to apply. The application is done online via i-Akaun and processing takes approximately 2–4 weeks. Note that EPF funds are disbursed directly to the relevant party (developer, seller, or bank), not to your personal account. For the full process, see our EPF Withdrawal Guide.

Start Your Property Search

Ready to take the first step toward owning your home? Browse affordable properties in popular first-time buyer areas on SuperHomes:

- Properties in Cheras

- Properties in Puchong

- Properties in Subang Jaya

- Properties in Shah Alam

- Properties in Setia Alam

- Properties in Kajang

- Properties in Rawang

- All Properties Under RM500K